How to Claim Life Insurance in Pakistan: Step-by-Step Process Without Delays

Filing a life insurance claim in Pakistan should provide financial relief during grief, not additional stress. Understanding the precise procedure under SECP regulations empowers beneficiaries to secure settlements efficiently. Follow this structured guide to navigate the claim process for your life insurance in Pakistan without unnecessary delays.

Step 1: Immediate Notification (Within 48 Hours)

Time is critical. Notify the insurance provider within 48 hours of the policyholder's death. Most companies maintain 24/7 helplines and online portals for initial intimation. Have the policy number, the deceased's full name, the CNIC number, and the date of death ready. Request a claim reference number and ask for the complete document checklist specific to your life insurance policy type. Prompt notification triggers the insurer's internal timeline obligations under SECP guidelines.

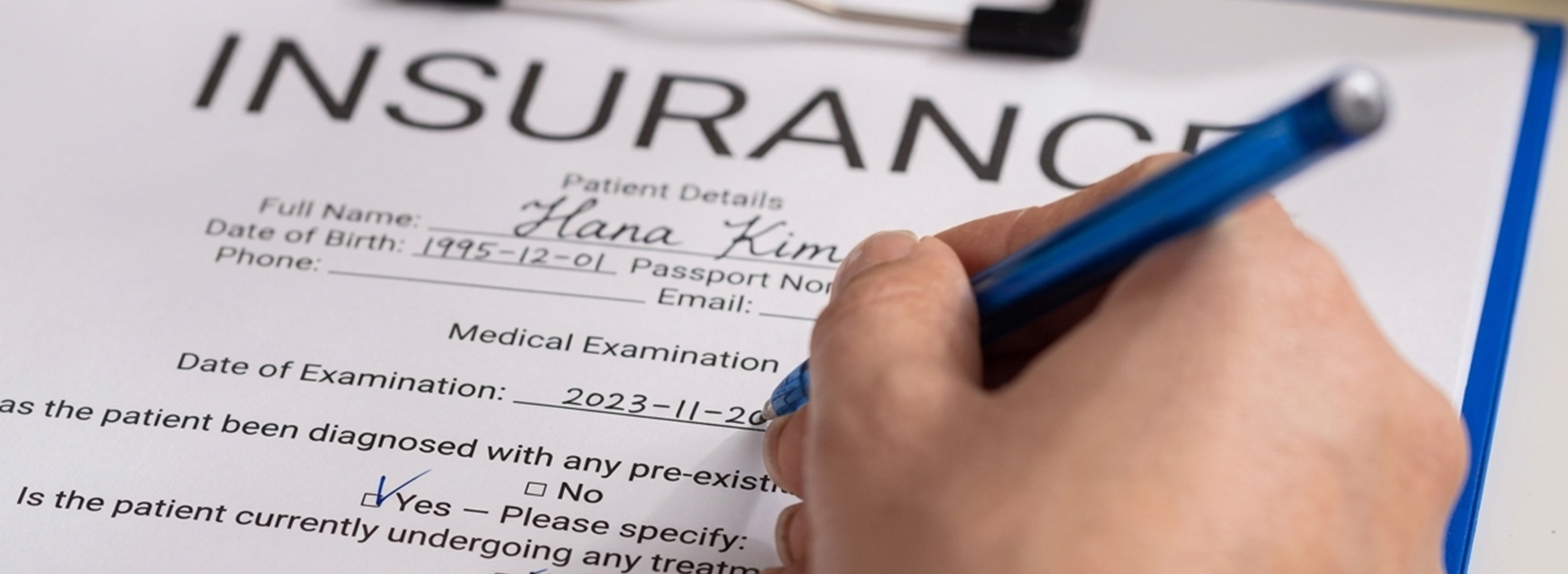

Step 2: Essential Document Preparation

Incomplete documentation is one of the most common causes of claim delays.

Gather these mandatory documents:

- Original policy document or certified duplicate copy

- Duly completed claim form (provided by insurer)

- Official death certificate issued by the Union Council or an authorized hospital

- CNIC copies of the deceased and all nominees

- Proof of nominee relationship (marriage certificate for spouses, birth certificates for children)

- Bank account details of the nominee on the bank letterhead for electronic transfer

- For accidental deaths: FIR copy and post-mortem report from authorized medical facility

Organize documents chronologically in a folder. Retain photocopies of everything submitted. For life insurance Pakistan policies, where death occurs within the first two policy years, additional medical records from treating physicians, and enhanced scrutiny are conducted during this contestability period.

Step 3: Accurate Form Completion

Complete the claim form truthfully and legibly. Discrepancies between application disclosures and actual circumstances trigger investigations that delay settlements by months. Ensure the nominee signs every page. If multiple nominees exist, attach a notarized affidavit specifying exact distribution percentages to prevent disputes. Never submit unsigned or partially completed forms; incomplete forms may result in processing delays or the return of documents.

Step 4: Formal Submission with Proof of Receipt

Submit documents physically at the insurer's head office or registered branch; avoid courier services for initial submission. Request a dated acknowledgment receipt bearing the processing officer's signature, designation, and unique reference number. This receipt is your legal proof of submission date. Under SECP regulations, insurers must acknowledge claim receipt within three working days and request additional documents (if needed) within 15 days of complete submission.

Step 5: Proactive Follow-Up Protocol

Passive waiting invites delays. Implement this follow-up schedule:

- Days 1–7: Confirm document receipt via SMS/email tracking systems

- Days 8–15: Contact the claims officer weekly for status updates

- Days 16–30: If additional documents are requested, deliver within 48 hours

- Beyond 30 days: Escalate to the branch manager, then the regional head, with your acknowledgment receipt

Under SECP guidelines, insurers are generally required to process complete claims within specified timelines, typically around 30 days. If delays occur, policyholders may consider submitting a formal written follow-up or escalation.

Avoiding Common Rejection Triggers

Life insurance Pakistan claims face rejection primarily due to:

- Material misrepresentation: Undisclosed pre-existing conditions or inaccurate health declarations during policy purchase

- Lapsed policies: Premiums unpaid beyond the 30-day grace period

- Nominee disputes: Unclear beneficiary designations or contested claims by legal heirs

Prevent these issues by maintaining accurate policy records, paying premiums promptly, and updating nominee details after major life events like marriage or childbirth.

Regulatory Safeguards for Claimants

SECP's Insurance Rules 2021 protect beneficiaries through:

- Mandatory three written reminders before policy lapse

- 30-day settlement timeline for complete claims

- Right to a written explanation for claim rejection

- Grievance redressal mechanism at SECP's Insurance Division within 60 days of rejection

Life insurance death benefits in Pakistan are generally exempt from income tax under current tax laws (subject to applicable regulations), allowing beneficiaries to typically receive the full amount.

Final Settlement Process

Upon approval, funds are transferred electronically to the nominee's verified bank account within seven working days. Insurers must provide a settlement statement detailing the approved amount and any deductions (e.g., outstanding policy loans). Retain this document permanently for tax and legal records.

Conclusion

A smooth life insurance Pakistan claim experience stems from preparation, not pressure. Maintain organized policy records, disclose all facts accurately during purchase, keep nominee details current, and act promptly after loss. The best life insurance Pakistan providers combine robust coverage with seamless claim settlement, but your diligence in documentation and follow-up remains the decisive factor. By mastering this five-step protocol, beneficiaries transform a potentially daunting process into a dignified transition toward financial stability during life's most challenging moments.

Eng

Eng  Login

Login